The recent appearance of the COVID-19 pandemic highlights the strong negative impact on the production of goods and services globally and exposes the high correlation of the economies between Europe, America and Asia. We are now faced with the unknown of the duration and magnitude of this contraction and how Mexico will respond at the level of its authorities and the population to this challenge.

The real estate sector, for its part, with its high contribution to GDP, whose decline is already forecast above the previous crises that affected this industry in 1995 and 2009, is an example of both supply and demand being affected. On the supply side we observe the clear disruption of supply chains, while demand exposes the brake on the mobility of goods and people and the measures applied to the confinement to households that directly affects the contraction of spending towards the basic goods.

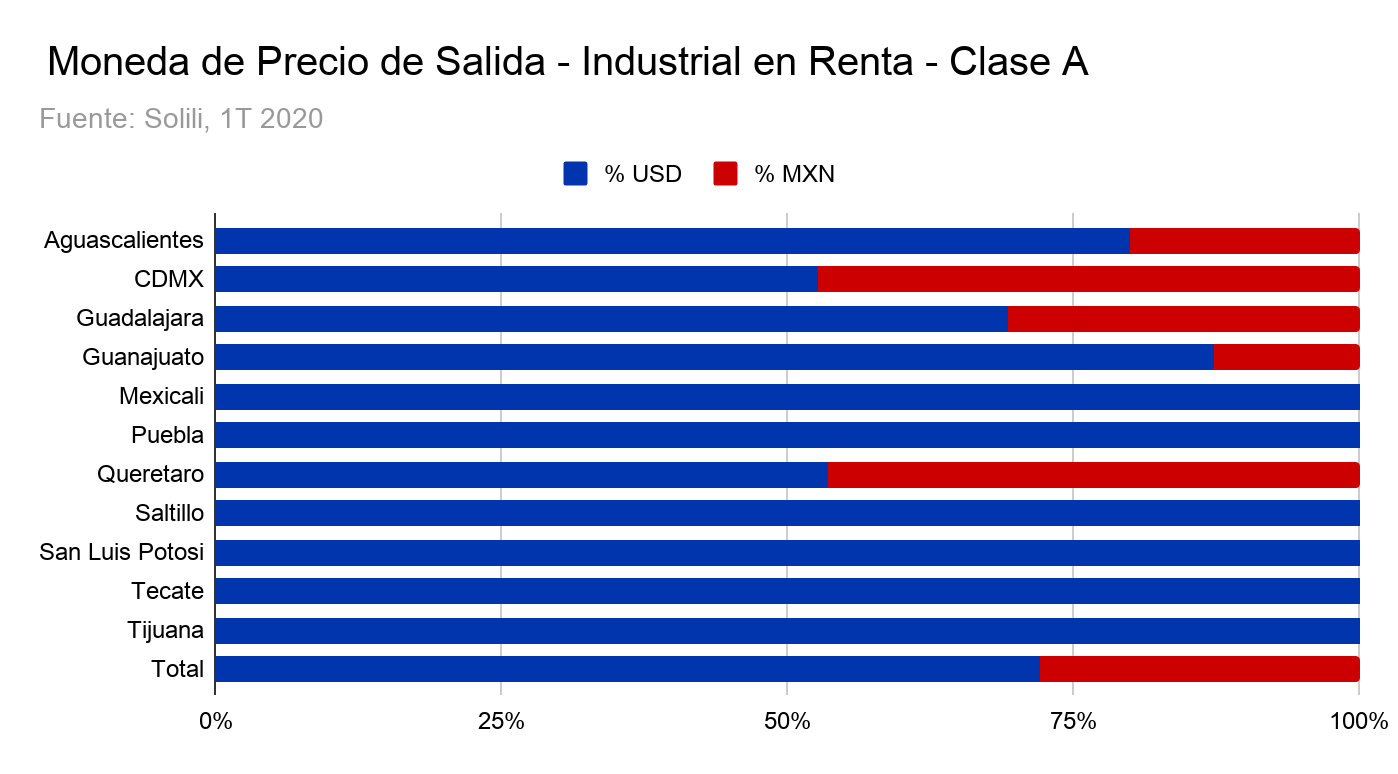

Another characteristic of real estate investment is the knowledge of the risks inherent in it, highlighting the exchange rate risk that we will analyze with the figures from the end of March issued by www.solili.mx with the main indicators of the corporate and industrial segments.

During the first quarter of the year, the Mexican peso depreciated on average 24.5% at the beginning of the quarter at 18.88 USD / MXN and ending on March 30, 2020 with 23.51 USD / MXN. As we observed in the analysis carried out, the office sector has a greater influence on its transactions in national currency, while a large majority of exit rental prices for the industrial segment are made in dollars, which gives greater protection to risk. exchange rate in the event of a depreciation of the Mexican peso.

At the other extreme, below the national average with 72% of the offers handled in dollars, we have Mexico City and Querétaro with 53% of dollarized offers and Guadalajara where this percentage reaches 69%, which exposes them with greater force to the volatility of the exchange rate in their incomes, since there is an important portion denominated in pesos.

As for class B and C, in general terms the offers are handled in Mexican pesos in almost all the cities of the country, which could be justified in that a majority of these inventories, over all Class C, correspond to less structured investors. and that they have very little offer compared to the rest of the national and foreign investors that dominate the market.

Monterrey, Querétaro and Puebla stand out with a majority of their Class A office offerings in local currency where 99%, 96% and 77% of the rental prices are managed in Mexican pesos, at the end of 1Q 2020, according to www. solili.mx.

Mexico has had macroeconomic stability in at least the last 20 years, and although the national currency has reported significant fluctuations, from this date to the present, it has never suffered such a sharp depreciation in such a short time. For agents involved in the real estate sector this can be seen positively since the exit prices of properties that are in national currency have become more competitive with respect to those that are in US dollars, making them more attractive. this type of space for investors

Stay up to date with the most important news to the real estate

Subscribe Solili Newsletter