At the end of June 2020, the country was undergoing the complex adaptation to the new order of activities in the midst of the health alert due to the increase in infections while productive activities gradually changed from red to orange, in several cities nationwide. Uncertainty again affects the national economic sector, where a contraction of the Gross Domestic Product (GDP) in Mexico of approximately 10% by 2020 according to the International Monetary Fund (IMF) is expected, in the scenario of continuous demands on the federal government so that it implements innovative public policies that maintain and encourage the investments that had come to the country in recent years.

In turn, industrial real estate investment worldwide has been influenced by the redefinition of supply chains in production, and in the particular case in Mexico that was emerging with a significant advance in the sector's institutionality. Under this scenario, industrial developers face a panorama marked by the recovery of industrial demand and the key is once again to restore the confidence of both consumers and investors in the country. On the other hand, the implementation of the Treaty between Mexico, United States of America and Canada (T-MEC) opens for Mexico an important opportunity for industrial investments seeking to mitigate the effects of the pandemic in the medium term.

The main Mexican cities have industrial markets that result from a combination of manufacturing and logistics. The manufacturing sector has increasingly resented government regulations to prevent the spread of the coronavirus. The collapse of the value chain, the paralysis of production and the decrease in consumption has caused that the companies dedicated to manufacturing have stopped growing and with it companies of this type demand lower volumes of industrial space. The opposite has been the behavior of the logistics industry that has continued to grow and as a consequence of this impulse the demand for space to carry out this type of activities has been increasing. For this reason, markets with a high presence of manufacturing activity such as San Luis Potosí, Aguascalientes, Guanajuato, Tecate, Mexicali, Saltillo and Puebla have been affected more strongly, those with a mixed structure such as Monterrey, Guadalajara, Tijuana and Querétaro have felt less measure, while where there is greater participation of the logistics sector, developers are on the way to reversing the turning point that began with the appearance of Covid-19, as is the case of the Metropolitan Area of Mexico City.

At the end of 2Q 2020, there was little growth in inventory at the national level, if we compare it with the average observed in previous periods, in which growth rates were around 5%. In relative terms, their inventories Guanajuato, Aguascalientes and Guadalajara increased by 4%, 2.1% and 1.8%, respectively, with Guadalajara closing this quarter about 60 thousand m². The rest of the cities were below 1% with little incorporation of new industrial buildings into the inventory, and some cities such as Puebla and Tecate did not complete works during the quarter. Monterrey highlights that in the second quarter of 2020 it reported the completion of seven buildings, mostly class A and BTS type, which totaled close to 112 thousand m², increasing its inventory by 1%. The national panorama as a whole was the result of the total paralysis of activities of the first two months of the period that gradually resumed the start during the month of June 2020, which resulted in the majority of the projects postponing delivery dates. and that industrial developers will act cautiously in the face of the uncertainty that exists.

Table 1: Indicators of the Industrial Real Estate Market in the Second Quarter of 2020 in the Main Markets of Mexico.

Source: Solili, July 2020.

Regarding the vacancy rate in general terms, the market continues to present healthy figures, being the best positioned commercial real estate segment of all in this indicator. The markets of Mexicali and Tijuana reflect the lowest vacant percentage at the national level with 2.3% and 2.5%, respectively. For its part, Guanajuato, the main bajío market, closed with a vacancy rate of 7.4%, which although it is the highest in the country's industrial markets, shows a slight downward trend and remains at very healthy levels.

Aguascalientes registered the highest downward adjustment of the vacancy rate relative to its inventory by more than one percentage point compared to the previous quarter, and finally San Luis Potosí closed at 4.9%, with a slight upward trend compared to 1Q 2020. The The rest of the main mixed industrial markets, which combine manufacturing and logistics at the end of 2Q 2020 such as Mexico City, Monterrey, Guadalajara and Querétaro, also increased their vacant spaces and closed the quarter with 3.1%, 5.5%, 5.4% and 3.6% , respectively.

Map 1: Volume of Industrial Vacancy in the Main Markets of Mexico.

Source: Solili, July 2020.

The majority of rental prices reflected slight increases with respect to the quarter derived from the appreciation of the Mexican peso against the US dollar. Price changes this quarter were not abrupt and range from the largest upward adjustment with 22 cents in Monterrey to the largest downward adjustment of 11 cents in Mexicali, generating a market without major surprises in rental prices. , a situation that could be sustained in the future as long as institutional developers maintain a balance between supply and demand, in a market where vacancy plays in favor.

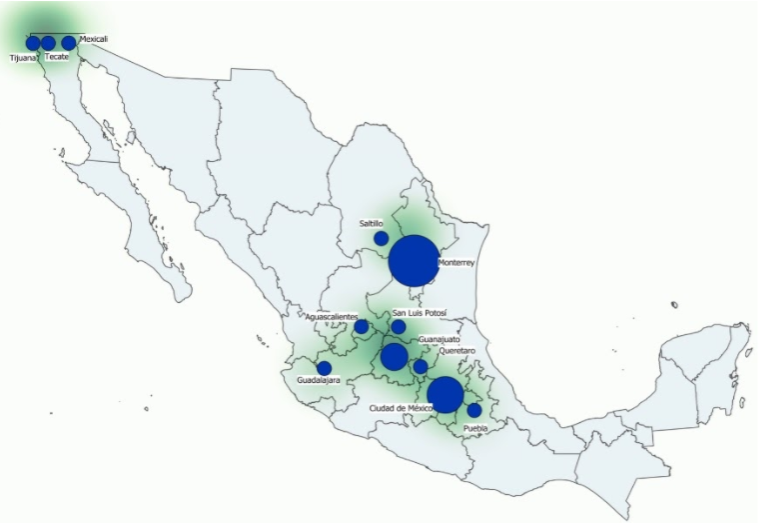

An indicator that projects the developer's expectation in view of the environment it envisions is the start of construction that for this second quarter of the year and despite two months of closing the works, we saw it moving in Mexico City, Monterrey, Puebla, Tecate, Guadalajara and Tijuana.

Map 2: Volume of Industrial Construction in the Main Markets of Mexico.

Source: Solili, July 2020.

The Metropolitan Area of Mexico City initiated two new speculative projects that together add up to a profitable area of 66 thousand m², while Monterrey with seven new projects started total about 93 thousand m², 74% speculative but which produced a quarterly contraction of the 9% and 12% annually in this active market. Tijuana, which perceives the attacks of being a border city, began construction of three projects totaling 28,000 m², maintaining levels similar to the previous quarter, even with the two-month paralysis that the building. In Puebla, Q2 2020 began the construction of a custom-made project (BTS) for a company in the food and beverage sector in the Huejotzingo corridor with a very important amount for this market, where the total volume of works under construction doubles. compared to the previous quarter. In Tecate all the developments are of the speculative type and this quarter a 5.2 thousand m² warehouse with a profitable area began construction on the Tecate-Tijuana corridor.

Guadalajara, despite the inactivity of two months in construction, was driven by the development of a tailor-made project in the El Salto corridor, in addition to others that began construction despite the panorama of uncertainty through which it transits the country. However, in other cities there was no start of construction such as San Luis Potosí, Saltillo and Mexicali, where developers delayed the start of some speculative projects that they planned to start this quarter, but given the situation of uncertainty they decided to put them on pause and resume them once the situation is more clearly perceived in the near future. The Querétaro panorama closes, despite having reported higher volumes than in the previous quarter and in 2Q 2019, the developers have remained cautious before the start of new projects with the expectation about the behavior that the demand could have and based on that they planned the emergence of new industrial developments.

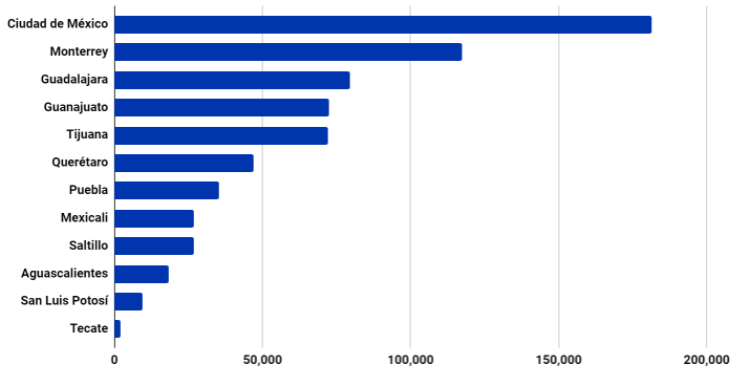

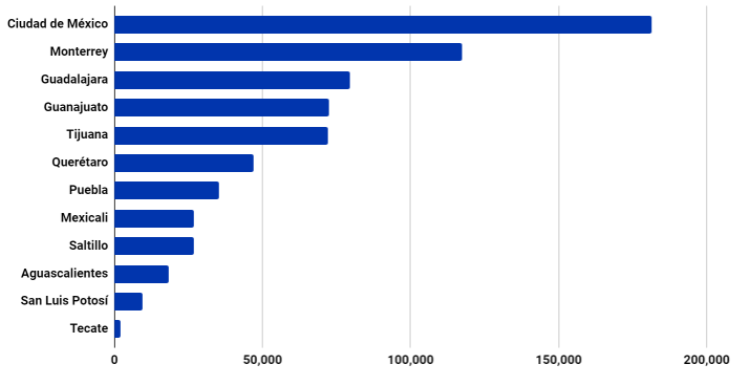

Graph 1: Gross Industrial Demand as of 2Q 2020 by Main Markets of Mexico (m²).

Source: Solili, July 2020.

Analyzing the gross industrial demand at the national level, we will be able to understand the correlation of factors that allow us to infer the trends in each market. In the Metropolitan Area of Mexico City, gross demand reported 181 thousand m² in a market that indicates high volumes of unemployment, in the order of 125 thousand m², which affects the sharp decrease in net absorption, despite being This is a market where there is a strong logistics component. A trend that was developing prior to the pandemic and later reinforced, was to offer industrial spaces closer to the city center, to satisfy the demand of e-commerce companies that see corridors such as Vallejo, Naucalpan and Iztapalapa advantageous locations for your distribution centers.

Monterrey with almost 20% of the industrial inventory nationwide has remained one of the cities in the country with the highest demand for industrial space during the pandemic period. The variety in terms of infrastructure and supply offered by the market has allowed a sustained performance of the leasing activity, which in this quarter reached almost 122 thousand m², highlighting industries in the logistics sector, industrial supply and the manufacturing sector. This amount represented a drop of 35% compared to the previous quarter and 48% compared to the second quarter of 2019, mainly motivated by the decrease in the volume of demand for manufacturing spaces, which went from representing about 70% to 30 % of demand, a negative effect that has been offset by the increase in investments by companies dedicated to the logistics sector.

Gross demand in Tijuana closed the quarter with 72 thousand m², representing a quarterly decrease of 57% and 40% annually, where the drop in leasing activity is a sign of a border market that resents the negative effects of the pandemic, the which were not so noticeable during the first quarter of the year. Among the companies installed during the period are companies from the medical device industry, the manufacturing sector, the rubber industry, packaging, the electrical industry and mainly the logistics sector.

Guadalajara at the quarterly end indicates a gross demand of almost 80 thousand m², standing at figures similar to those reported in periods prior to the pandemic, companies in the logistics and e-commerce sectors have boosted demand. On the other hand, the net demand reports a contraction of 81%, as a result of the high volumes of unemployment reported by this market, which amounted to a total of 48 thousand m².

In the second quarter of 2019, the case of the Puebla market stands out, where the gross demand of 35 thousand m² originates, mainly, with the construction of a custom-made project (BTS) for a company in the food and beverage sector on the corridor from Huejotzingo.

Despite the fact that the existing offer of industrial space in the city was only 65 thousand m², it is enough to satisfy a demand that has not yet taken off, however, the market should provide a diversified offer in size, location, characteristics , among others, to immediately satisfy the demand of companies seeking to establish themselves in the region. If not, it will be necessary to opt for tailor-made projects, a situation that for many companies is complicated when what they seek is to establish themselves immediately.

The industrial markets of the Bajío, characterized by the strong manufacturing vocation of most of its cities, were affected by the demand this quarter that ended. Guanajuato registered a gross demand of 70 thousand m² distributed in 15 transactions, with surfaces that average 4.6 thousand m², which mostly correspond to companies that will use logistics and storage spaces, and some correspond to the automotive industry. For its part, San Luis Potosí totaled almost 10 thousand m² of companies that are installed in the area and wish to expand to medium-sized spaces ranging from 4 thousand to 8 thousand m². San Luis Potosí exhibits a diversified industrial offer that ranges from 2,000 to 20,000 m², so the city has the ability to meet demands of various sizes, both in logistics and manufacturing. We closed with Aguascalientes that at the end of 2Q 2020 reflected a gross demand of 18.4 thousand m², in the Aguascalientes Sur corridor with a speculative ship, and in addition to this, the net demand reported positive figures, even in the midst of the adverse scenario it registered area.

Saltillo and Tecate also adjusted their gross demand downward by 60% and 43%, respectively. Saltillo registered a gross demand of 26.4 thousand m² with a strong manufacturing component, while Tecate reported the lease of a 1.8 thousand m² industrial warehouse located in the Mexicali-Tecate corridor. Mexicali also registered a contraction of 62% of demand with 25.5 thousand m² at the end of 2Q 2020, concentrating 46% of the demand on the Airport-Garita 2 corridor, the vast majority of these spaces corresponding to logistics and storage.

In general terms, the developers nationwide surveyed by Solili at the end of the second quarter of 2020 consider that the rental prices were and will remain stable in the scenario of moderate increases in the vacancy that they saw this quarter and that they foresee will continue. Regarding demand, if they consider that it moved between stable and with downward adjustments, but they are more optimistic towards the semester, which will combine this scenario with constructive activity that, once the start of activities is over, will tend to normalize.

Although we are facing a complex scenario shaped by the expectation of the presidential elections in the United States and the development of the growth of coronavirus infections in Latin America and Mexico, the institutional developers of the industrial real estate segment know the behavior of the market and cautiously measure the opportunity to continue building in response to the projection generated by demand and thus maintain a market where rental prices are stable and vacancy remains at healthy levels.

The lesson of other crises has shown that past critical moments, the recovery of investment resumes and even exceeds that of previous periods under the premise that the government and the private sector work together for the good of the population and the economy.

For the remainder of this year 2020 at Solili we anticipate that the markets will continue with vacancy indicators and stable prices, but with lower volumes of demand than those reported in previous periods, mainly due to factors such as the decrease in global manufacturing activity, decreases of Mexico's foreign trade, the contraction in consumption, the decrease in consumer confidence and the decrease in demand for semi-durable and durable goods in the short term. However, we have elements that we can consider positive in the medium term and which will be taking effect at the beginning of next year, which are the entry into force of the T-MEC, which opens the possibility for Mexico to develop as a manufacturing center in North America given the tariff advantages that this treaty will provide to export to the United States of America and Canada. Likewise, we consider that there will be an interest on the part of some companies now established in Asia to relocate to Mexico, seeing, among other benefits, staying close to the parent companies or where the final product is made.

The industrial real estate segment of the country, although it is going through times of challenges, has a solid scaffolding in the supply and demand part that will allow it to overcome this situation successfully, the elements that make it globally competitive remain and in some cases increase, therefore we estimate that the industrial segment will continue with sustained growth rates for 2021.

Stay up to date with the most important news to the real estate

Subscribe Solili Newsletter